9 Strategies to Stop Losing Customers to Payment Failures

Every month, SaaS companies lose between 2% and 5% of their subscribers not because those customers wanted to leave, but because a payment failed and nobody did anything about it. That is involuntary churn, and it is one of the most fixable revenue leaks in subscription businesses.

The frustrating part is how normal this has become. Founders see failed charges in Stripe, notice a wobble in MRR, then shrug and treat it like background noise. Bad idea. Payment failures are not random weather. They usually come from specific, repeatable causes like insufficient funds, expired cards, issuer outages, weak retry timing, or clumsy billing UX.

The good news is that solid payment failure strategies can recover a meaningful chunk of that lost revenue. Many subscription businesses recover 30% to 70% of failed payment revenue once they stop treating recovery like an afterthought.

This guide breaks down nine practical ways to stop losing customers to payment failures. No vague hand-waving. Just specific tactics you can implement, why they work, and what to measure so you know whether they are actually helping.

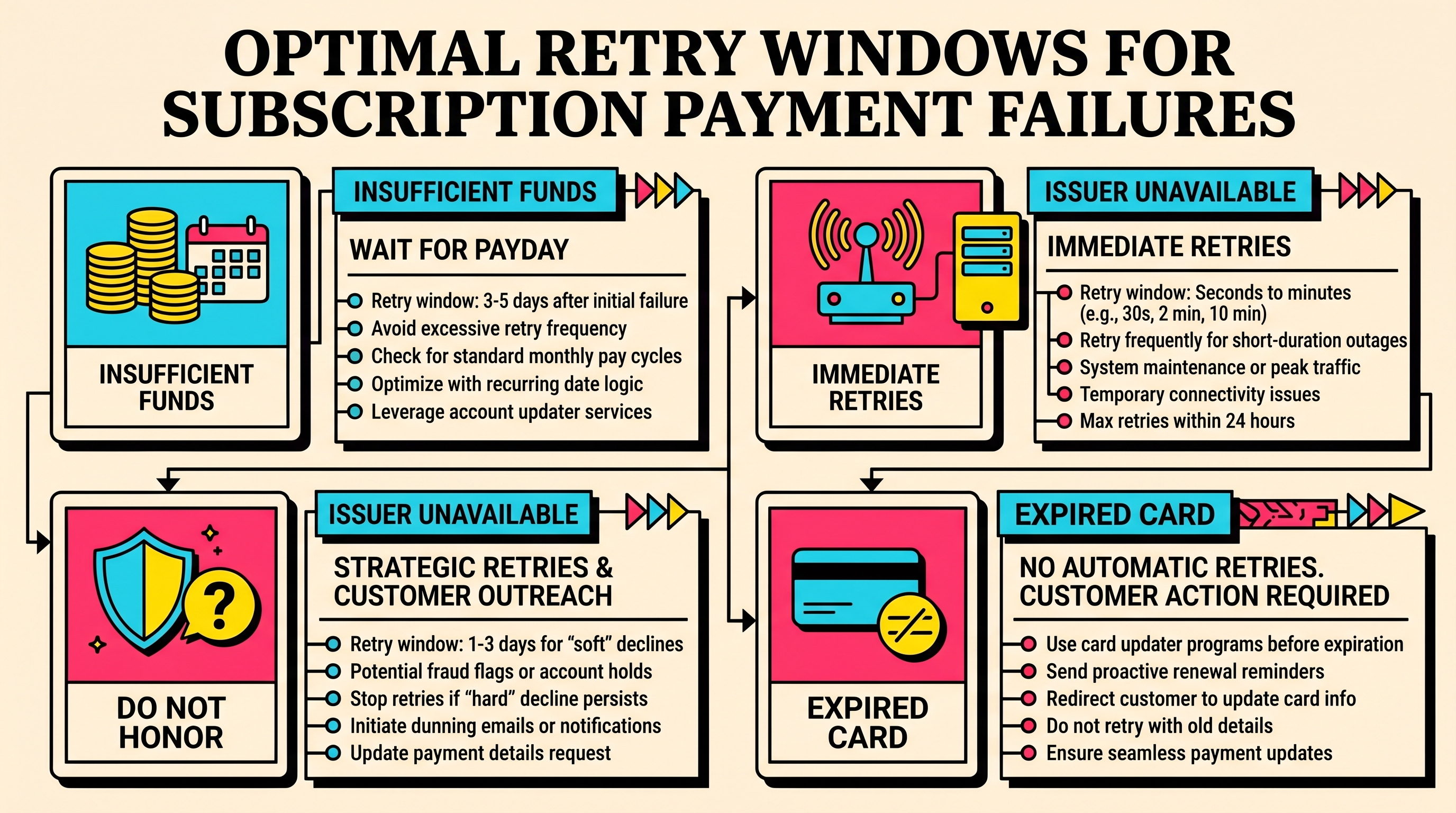

1. Implement smart retry logic that matches decline patterns

The default retry setup in Stripe is a blunt instrument. It is useful, but it is still generic. It treats a temporary issuer outage, an expired card, and an insufficient funds decline like they are cousins when really they need different follow-up.

Smart retry logic means timing retries around the reason the payment failed.

- Insufficient funds: Retry 2 to 3 days later, often around common payday cycles like the 1st or 15th.

- Issuer temporarily unavailable: Retry within a few hours. These failures often clear quickly.

- Do not honor: Wait a few days. Immediate retries usually do nothing except look desperate.

- Expired card: Do not keep slamming the same card. Push the customer into a card update flow.

Understanding Stripe decline codes and what they mean for your revenue is the foundation here. If you do not know which failure types are recoverable through timing and which need customer action, your retry system is basically just hopeful button mashing.

A simple rule set outperforms generic retries surprisingly fast. You do not need a PhD in payments. You need a shortlist of common failure reasons and a default action for each one.

What to measure: Recovery rate by decline code. If insufficient funds is recovering poorly, your timing is wrong. If expired cards are sitting in retry loops, your flow design is wrong.

2. Set up pre-dunning notifications before payments fail

Most teams only contact customers after a payment fails. By then you are already in cleanup mode.

Pre-dunning flips that. Instead of reacting after the charge breaks, you contact the customer before the next billing event when the risk is predictable.

The highest-value triggers are usually:

- Card expiring soon: Send a reminder 30 days before expiry, then again around 7 days before.

- Upcoming annual renewal: Warn customers before a larger renewal charge lands.

- Known payment method issues: If card checks suggest a problem, ask the customer to verify details before the next invoice.

This is why pre-dunning matters more than most SaaS teams realise. The easiest failed payment to recover is the one that never fails in the first place.

A good pre-dunning message is short, direct, and useful. Tell the customer what is likely to break, why it matters, and give them one clear path to fix it. Do not make them go on a billing settings treasure hunt.

What to measure: The percentage of expiring cards updated before renewal. If that number is low, you either are not notifying early enough or your update flow has too much friction.

3. Build a multi-channel dunning sequence

Email-only recovery is fine if you enjoy leaving money on the floor.

Even well-written transactional emails miss people. Some land in Promotions. Some get skimmed and forgotten. Some are seen after the account has already been paused. That is why multi-channel recovery usually beats email-only recovery by a wide margin.

A sane sequence looks like this:

- Day 0: Email plus an in-app banner.

- Day 3: Follow-up email with a direct update link.

- Day 5: SMS or push notification if you have the channel.

- Day 7: More personal message from a real human address.

- Day 10+: Final warning before restricted access or pause.

The trick is not to become annoying. The trick is to be impossible to miss without sounding like a collection agency. The customer should always know three things: the payment failed, their account is still recoverable, and fixing it is easy.

In-app messaging matters a lot here because active users are your easiest recoveries. If they are literally inside the product while their subscription is failing, that is the moment to make the next step stupidly simple.

What to measure: Recovery rate by channel and by sequence step. If almost all recoveries happen after the first email, great. If in-app banners are outperforming everything else, lean harder into them.

4. Offer alternative payment methods at the point of failure

When a card fails, most SaaS products say some version of “please update your card.” That is only half useful.

Sometimes the problem is not the specific card details. Sometimes the customer’s bank keeps flagging recurring charges, the card is being replaced, or the company prefers a different rail entirely. If the only recovery option is “try another card,” you are narrowing your odds for no good reason.

Depending on your market, useful alternatives can include:

- ACH or bank debit for US customers.

- SEPA Direct Debit for European customers.

- Digital wallets where appropriate.

- Link by Stripe or other lower-friction saved payment options.

Alternative methods do two things. First, they give customers another path to stay subscribed right when friction is highest. Second, they reduce your long-term dependency on card networks, which are the source of a lot of involuntary churn in the first place.

This matters most if you have larger annual contracts, B2B customers with procurement quirks, or geographies where cards are not the cleanest recurring payment rail.

What to measure: How often recovered customers switch payment method during recovery. If that number is meaningful, alternative methods are not optional. They are doing real work.

5. Use account updater services aggressively

This one is as close to a free win as payments gets.

Card networks and processors can often update stored card details when a customer gets a replacement card because of expiry, loss, fraud, or routine reissue. Stripe supports automatic card updating for many networks, which means a decent share of would-be failed renewals can be avoided without the customer doing anything.

You still need to verify that this is working the way you think it is.

- Check that automatic updating is enabled where supported.

- Monitor how many expired-card failures still slip through.

- Combine account updater with expiry reminders instead of assuming the updater catches everything.

A lot of founders hear “automatic updater” and mentally file the problem away forever. That is how you end up discovering three months later that your expired-card churn is still ugly because a meaningful segment of cards never updated automatically.

The right mindset is simple: let automation catch what it can, then build a backup path for the cases it misses.

What to measure: Expired-card failure rate before and after verifying updater behaviour. If it barely changes, something in your assumptions is off.

6. Optimize your billing timing

Billing timing gets ignored because it sounds small. It is not.

When you charge, retry, and escalate can meaningfully affect payment success. Cash flow patterns, bank behaviour, and customer attention all matter.

A few practical timing rules:

- Charges near common pay cycles often perform better than awkward mid-cycle dates.

- Mid-week attempts usually outperform weekend retries.

- Morning retries tend to do better than late-night retries in many markets.

- If a charge fails on a Friday, retrying on Saturday is often dumb. Waiting until early the following week can produce a better hit rate.

This is the same thinking behind setting up a proper Stripe payment recovery flow. A recovery system is not just what you send. It is when you send it and when you try again.

If customers can choose their billing date, that gives you another lever. If they cannot, segmenting retry timing intelligently still helps.

What to measure: Failure rate and recovery rate by billing date, day of week, and retry window. If timing does not matter for your business, great. But test it before assuming that.

7. Implement grace periods instead of immediate cancellation

Immediate cancellation after a failed payment is one of the dumbest self-inflicted wounds in SaaS.

A failed payment is not always a churn decision. Sometimes it is a temporary bank issue, a card replacement, a company purchasing delay, or a customer who just missed the first email. If you cut access instantly, you turn a recoverable billing issue into a real retention problem.

A better approach is a structured grace period:

- Days 1 to 7: Full access, visible reminders, easy update path.

- Days 8 to 14: Limited access to non-essential features.

- Days 15 to 30: Read-only access, with billing recovery still easy.

- After that: Pause the account instead of deleting history.

This works because it respects the customer’s existing investment in your product. Their data is still there. Their workflows are still there. Fixing the card gets them back to normal quickly.

It also gives your recovery system time to work. Smart retries, multi-channel reminders, and manual outreach are all useless if your product slams the door immediately.

What to measure: Recovery rate by grace-period stage. If most recoveries happen in the first week, perfect. That still proves the grace period is earning its keep.

8. Personalize recovery based on customer value and activity

Not every failed payment deserves the same treatment.

A $29 per month self-serve account and a $2,000 per month account with heavy product usage should not go through identical recovery paths. That is not cold-hearted. It is operational common sense.

High-value accounts can justify personal outreach. Mid-market customers might warrant a stronger email sequence plus faster escalation. Lower-value self-serve customers should still get a great automated path, but not necessarily manual intervention.

Activity matters too. A customer who logged in yesterday and then had a payment fail is a far better recovery candidate than one who has been inactive for two months. Usage is intent. Treat it that way.

This segmentation lets you spend time where it compounds instead of pretending every account should receive white-glove recovery treatment.

The mistake here is overcomplicating it. You do not need a giant scoring model. A few practical segments based on MRR, plan type, and recent activity will already improve your prioritisation.

What to measure: Recovery rate by customer segment. If your high-value accounts are recovering poorly, that is a serious operational miss.

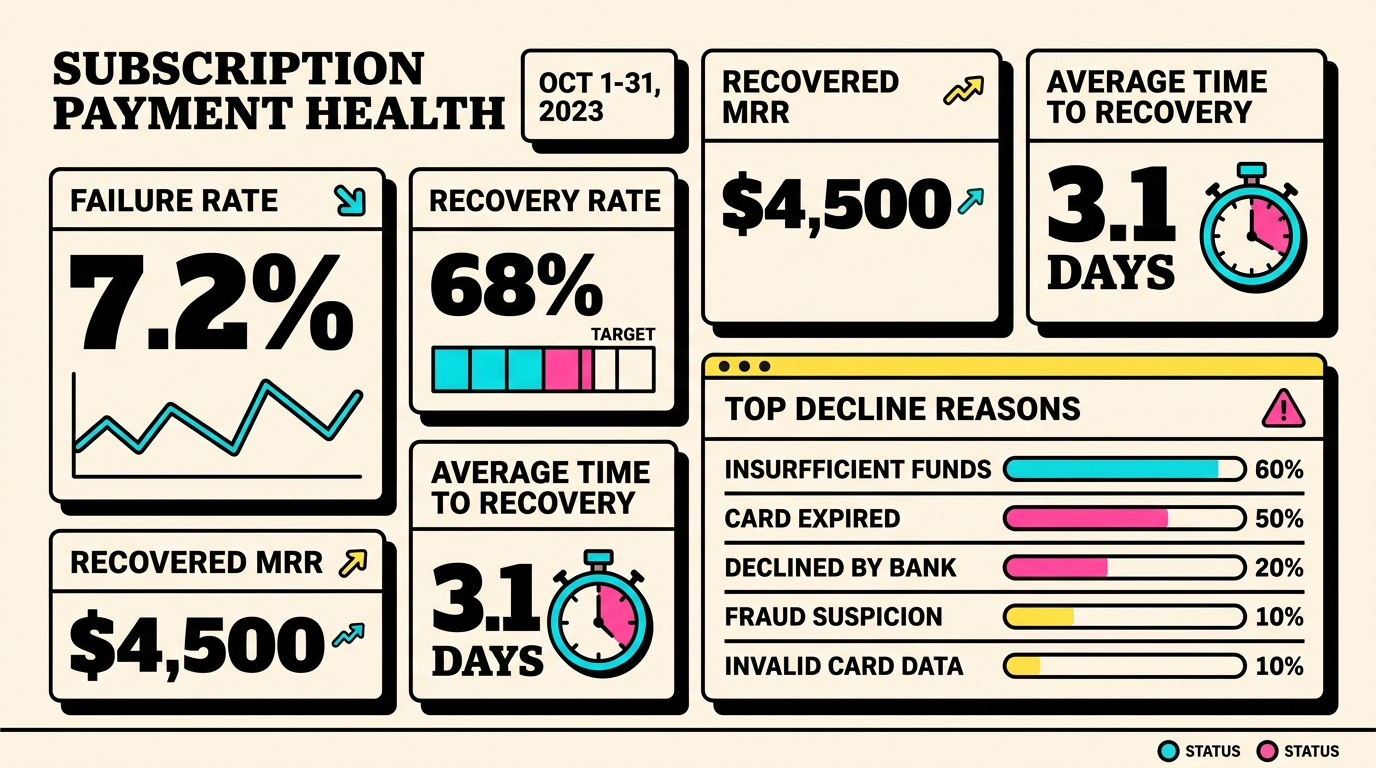

9. Review payment health metrics every week

The final strategy is the least sexy and maybe the most important: actually watch the system.

If you review payment health monthly or quarterly, you are learning too slowly. A weekly review is enough to catch spikes, broken flows, and recovery leaks before they quietly turn into a proper revenue problem.

Track at least these:

- Overall payment failure rate

- Recovered MRR vs failed MRR

- Recovery rate by decline code

- Average time to recovery

- Sequence performance by step and channel

- Expired-card share of failed payments

A weekly review keeps the whole machine honest. You will see if retry timing has degraded, if one message has stopped converting, if a billing change caused a spike, or if a specific decline type is suddenly hurting you more than usual.

That habit matters more than fancy tooling. Spreadsheet, dashboard, internal report, whatever. The format is not the point. The recurring review is.

What to measure: Month-over-month recovery rate and net involuntary churn. That is the number that tells you whether the system is genuinely improving.

Putting the system together

These payment failure strategies work best together, not as isolated tricks.

A sensible implementation order looks like this:

- Stop immediate cancellation with a grace period.

- Improve retry logic by decline reason.

- Add pre-dunning for predictable failures.

- Tighten your multi-channel recovery sequence.

- Verify account updater coverage.

- Expand payment method options where relevant.

- Tune billing timing and escalation rules.

- Add value-based segmentation.

- Review metrics every week and keep iterating.

That order matters because it tackles the biggest leaks first. Grace periods buy time. Smarter retries recover easy wins. Pre-dunning reduces preventable failures upstream. The rest compounds.

The bottom line is simple: involuntary churn is not just the cost of running subscriptions. A meaningful share of it is fixable. Every recovered payment is revenue you already earned and get to keep without spending another dollar on acquisition.

If you want to see where your Stripe setup is leaking revenue, run a free churn audit at https://churnbot.co/audit. It is the fastest way to spot failed payment recovery gaps before they get expensive.

Related Posts

7 Failed Payment Segments Every Stripe Team Should Track

Pre-Dunning: How to Prevent Failed Payments Before They Happen

Payment Gateway Decline Reasons Beyond Stripe

How healthy is your Stripe account?

Get a free churn health report. Find pending cancellations, failed payments, and expiring cards putting your MRR at risk.

Run Free Audit